The Air France case

In 2008, the fall in the price of a barrel of oil (from $145 to $45 in just a few months) could have been excellent news for Air France: for airlines, fuel purchases represent the second-largest expense item, after personnel costs. And fuel prices are closely linked to oil prices.

However, the opposite was true: Air France has recognized very substantial losses, due to the fall in oil prices. Out of a pre-tax loss of 1.2 billion euros, the effect is just over 700 million euros.

| Extract from the Air France - KLM reference document (financial statements at March 31, 2009) | Comments |

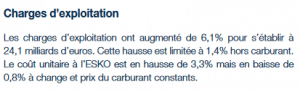

| Despite a slight fall in sales, operating expenses increased, with fuel costs the main item on the rise. ESKO: Equivalent Seat Kilometer Offered |

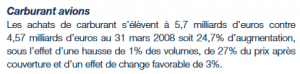

| Fuel costs rise "after hedging", while prices fall... |

How is this possible?

In fact, Air France's policy was to buy future to cover its fuel needs. In other words, Air France paid for its fuel at the price of previous years. If prices rise, Air France benefits from a competitive advantage, paying less than the market. But if prices fall, the opposite is true. Can such a strategy be described as hedging?

A hedging strategy consists in protecting the margin, not a single income statement line (in this case, purchases). If Air France has already sold the tickets, sales will not budge, and it is important to fix expenses too. In this case, the fuel must be bought forward to cover the margin. But if Air France sets the price of its fuel when the tickets have not yet been sold, then its selling price is constrained by a fuel price fixed in advance, which does not correspond to market conditions. This situation can be favorable if the price rises, or unfavorable if it falls.

This strategy, which is not immune to changes in market conditions, is in reality a gamble: Air France was betting that the price of oil would rise. It was a winning bet... until it turned out to be a losing one.

After the drop in the price of oil, Air France liquidated its positions, which increased its fuel costs for the current year, but enabled it to start off on the right foot and benefit from the new prices, like its competitors.

Subsequently, the Group modified its forward fuel purchasing strategy, limiting it to a shorter time horizon. Tickets not yet sold should not be hedged, but sold at a price that reflects conditions on the day of sale.

Conclusion: if a company's results depend on market conditions, it cannot be said to be hedged. Air France's "hedging" strategy was not really a hedging strategy.

[Back to main article: Understanding the negative price of oil]

For more information, please contact us!